Health savings accounts (HSAs) are special tax-advantaged savings accounts that allow U.S. taxpayers to pay for eligible health expenses with pre-tax dollars. And with the costs of daily life increasing, it’s no surprise that consumer adoption of HSAs is also on the rise. According to Morningstar, total HSA assets hit $146 billion in 2024, and up to four million new accounts could come online as a result of 2025’s “Big Beautiful Bill.”

Along with the flexible spending account (FSA), the growing HSA market represents an opportunity for merchants in health-related verticals to capture spending made using HSA and FSA debit cards. But there’s a problem.

Despite their growing use, HSA and FSA transactions are often a headache for merchants and their end customers — mostly because of the strict rules governing purchase eligibility. That causes unnecessarily high decline rates that make HSA/FSA payments frustrating at best and a serious gap in service quality at worst.

Let’s take a closer look at why unnecessary HSA/FSA declines happen so frequently, what steps your merchants can take to reduce them, and how the right payments technology partners can help ensure more of these transactions go through successfully.

The Problem: Too Many HSA and FSA Card Transactions Fail

HSAs and FSAs both provide end users with a way to pay for eligible healthcare expenses using pre-tax dollars. That reduces the effective cost of those expenses by the user’s marginal tax rate — a significant saving. HSAs also offer tax-free growth on investments made with the accounts, adding an additional layer of tax relief.

In both cases, the account holder is issued a payment card that they can use online or in store like any other debit card. But there’s one big caveat: HSA and FSA cards will decline any payment that isn’t being made for an eligible purchase or with an eligible merchant.

That decline is governed by IRS guidelines and industry standards maintained by the Special Interest Group for IIAS Standards (SIGIS). SIGIS oversees the technical standards for Inventory Information Approval Systems (IIAS), which are the systems used to verify whether items qualify for HSA or FSA purchase at the point of sale.

These standards are designed to ensure compliance and protect the tax-advantaged status of HSA and FSA programs. However, in today’s complex, sometimes overlapping, retail and healthcare environments the way eligibility rules, merchant category codes and payment system logic interact can sometimes result in legitimate transactions being declined.

The Many Reasons Legitimate HSA and FSA Transactions Get Declined

Why are so many legitimate HSA and FSA transactions declined? Ultimately, it comes down to an incompatibility between traditional payment systems and the rules surrounding the programs.

Reason 1: The Merchant Sells in a Mixed Retail Environment

There are many merchants who sell HSA/FSA-eligible healthcare products, but also other HSA/FSA ineligible merchandise. If the seller’s merchant category code (MCC) isn’t one of the handful approved under HSA/FSA, there’s a high probability the transaction will be blocked. Additionally, FSA account issuers can set account-specific MCC restrictions, leading to additional cardholder confusion in mixed-retail settings.

Pharmacies embedded inside local grocery or department stores, wellness retailers and even convenience stores selling common OTC medicines, like Advil, are examples of mixed merchants that may see their customers’ HSA and FSA cards regularly declined.

Reason 2: The Merchant Doesn’t Have a Compatible IIAS

Inventory Information Approval Systems (IIAS) are a way for merchants with ineligible MCCs to submit transaction data that proves an item being purchased is HSA- or FSA-eligible, allowing the transaction to be approved.

This should be a simple solution, but there are many reasons why a merchant might not have a compatible IIAS, including:

- The merchant’s processor forces them to use a proprietary and high-cost IIAS solution

- Adequate support for IIAS use isn’t available to the merchant, or they don’t know the solution exists

- The merchant’s processor or software platform does not offer an IIAS at all

Reason 3: Even Eligibility Exceptions Can Be Hard to Apply

In some cases, merchants may qualify for HSA and FSA acceptance even if their MCC is not on the standard approved list. For example, under what is commonly known as the 90% rule, merchants whose sales are made up primarily of HSA/FSA-eligible items can still be considered eligible without implementing a full IIAS.

However, qualifying under the rule and applying it successfully are not the same thing. If a merchant does not have a reliable way to track and document that at least 90% of their sales are eligible, or if their processor and payment systems cannot validate that status during authorization, legitimate HSA and FSA transactions may still be declined unnecessarily.

The good news is, SIGIS supports a fairly simple member registration process to help improve acceptance in approved merchant environments. Unfortunately, only limited MCCs are covered by this solution.

Reason 4: Custom Building HSA/FSA Compliance Into Software Platforms Is Expensive and Difficult

Most merchants today use some type of operational software to run their businesses, including their sales. The problem arises when merchants in non-medical MCCs run their operations on generic or non-medical software.

Custom building an IIAS into a platform is an expensive and time-consuming endeavor. Worse still, the ongoing compliance burden that comes along with anything related to medical sales and medical data is enormous. As a result, many software companies just don’t build HSA/FSA compliance into their platforms. That leaves merchants stuck between completely overhauling their tech stack or losing out on important HSA/FSA sales.

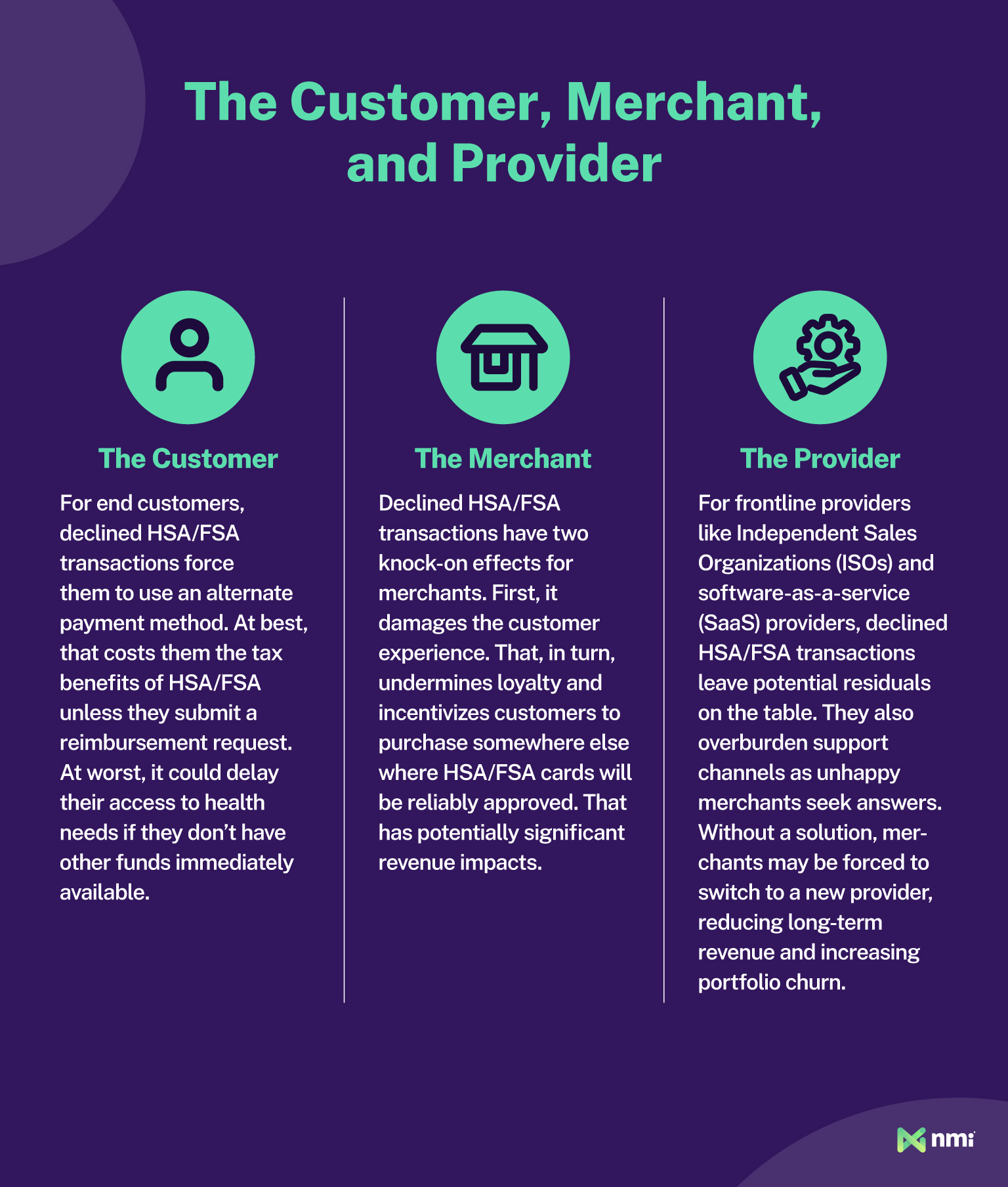

The Impacts of HSA/FSA Declines on Every Layer of the Transaction

The Solution: Best Practices for Supercharging HSA and FSA Approval Rates

If you have merchants selling in the health and wellness industries, there’s a good chance some are already running into problems with HSA and FSA declines. So, with that in mind, what can you do to help maximize their approval rates, simplify their operations and keep their customers happy and loyal?

The following are four best practices you can follow in order to offer your merchants the most frictionless HSA and FSA approvals possible.

1) Don’t Lock Merchants Into Proprietary IIAS Systems

Your merchants should have the ability to choose to use their own IIAS systems. Rather than locking merchants into a single, mandated system, find a technology partner who supports HSA and FSA through seamless integration of multiple third-party or even custom-developed IIAS solutions.

By giving merchants the flexibility to choose, you ensure they can minimize costs and integrate the IIAS they’re comfortable using or already have. That greatly reduces the likelihood they’ll jump ship in order to access a more flexible HSA/FSA solution.

2) Ensure Both Card-Present and Card-Not-Present Capabilities are Available

While in-person purchases were the original introduction for the HSA/FSA cardholders to use these benefits, today spending happens more often online. eCommerce has become an integral healthcare payment acceptance channel. Many consumers opt to make healthcare-related purchases online, and need a way to use their HSA and FSA cards.

If your merchants are only accepting in-person transactions, they are likely missing out on a growing number of revenue opportunities. To maximize sales, online FSA and HSA payments are a must.

3) Use Enhanced MCC Logic to Maximize Approvals in Mixed Environments

One of the biggest reasons HSA and FSA payments are declined is that traditional payment systems fail to identify and validate merchant eligibility in complex scenarios. Look for a solution that offers enhanced MCC logic that can identify eligibility in merchants with multiple codes.

Enhanced MCC logic offers a higher approval rate, maximizes revenue and eliminates the need for customers to split purchases across multiple cards. It also reduces the number of customer support calls your team has to manage from merchants who are confused about why certain transactions are being declined and not others.

4) Ensure Accurate, Reliable Handling of Auto-Substantiation Data

Auto-substantiation is the process of validating transaction data and passing it to the processor to ensure approval, either through an IIAS or through the 90% rule. Without auto-substantiation capabilities, a merchant’s IIAS won’t be useful, and transactions will likely be declined. To maximize approvals, ensure you’re working with a technology partner who supports full auto-substantiation and can accurately, reliably and automatically pass transaction validation data or 90%-rule exemptions to your processor.

Better HSA and FSA Processing Through Third-Party Tech Providers

A lot of merchants struggle with HSA and FSA declines because of the inherent complexity of the programs’ rules. But the good news is that offering your merchants a solution to their HSA/FSA problems doesn’t have to be difficult, time-consuming or expensive.

Whether you’re an ISO serving merchants in health, wellness or mixed niches or a SaaS provider with software for users that sell HSA/FSA-eligible products and services, your payments technology partner is your first stop for boosting approval rates. With the right partner, successfully processing eligible HSA and FSA transactions can be as easy as accepting any other payment.

NMI now offers our partners turnkey HSA/FSA processing that boosts approval rates and revenue for eligible transactions, both online and in store. If you’re ready to find out more, reach out to a member of our team.