Taking on merchant risk can open the door to higher residuals and greater control over pricing — especially for payment companies like wholesale independent sales organizations (ISOs) and payment facilitators (PayFacs). But with that opportunity comes a critical responsibility: underwriting.

Traditionally, manual underwriting has been slow and prone to error. Now, automated systems are redefining the way companies handle this process. By using advanced tools like automated risk scoring, companies can accelerate decisions, strengthen compliance and create a more reliable process from start to finish.

So, let’s break down what risk scoring is, how it works and why the right automated systems are so impactful for payments companies.

What Is a Risk Score?

A risk score is a metric that indicates how risky a merchant is. It’s typically presented as a simple, at-a-glance number, generally out of 100. Risk scores accomplish two goals in automated underwriting:

- They distill the results of a complex underwriting process, which involves potentially 100 or more checks, and thousands of data elements, into an instantly understandable number that underwriters can use as a quick jumping-off point for decisions

- They make automated decision-making possible by using pre-set thresholds. Human underwriters can adjust cutoffs based on their company’s risk tolerance and needs. Then, depending on where a merchant’s risk score falls in relation to the threshold, their account can be automatically approved, declined or quarantined. For example, any risk score above 50 could be set to auto-approve unless other high-risk indicators are identified.

Why Is Risk Scoring So Important?

In the modern payments space, risk scoring is a critical tool for combating fraud and optimizing the merchant experience. Some of the reasons risk scoring is such an important part of underwriting include:

- Growing complexity of fraud: Fraud tactics are evolving at an unprecedented pace, with criminals increasingly leveraging advanced technologies — including AI — to launch more sophisticated, adaptive attacks. At the same time, compliance requirements are also becoming more demanding and nuanced. This dual pressure makes effective and consistent due diligence far more challenging for human underwriters alone. Risk scoring — and automated underwriting in general — equips payments companies with the speed, consistency and intelligence they need to stay ahead of increasingly complex, AI-enabled fraud threats while meeting regulatory expectations

- The need for faster approvals: Underwriting is traditionally one of the biggest bottlenecks in account approval. Today’s merchants are focused on speed and convenience, so anything that helps underwriters approve merchants faster makes a big impact

- Support for rapid scaling: Automated risk scores and underwriting tools make it possible for payments companies to rapidly scale up. Without them, the volume of merchant applications would overwhelm manual review processes

- Stronger audit trails: When fraudulent merchants inevitably misbehave, processors, banks and even regulators want to see an audit trail to ensure proper vetting was done before approval. Risk scores add additional data points to the audit trail, and the automated underwriting system logs every check and every flag that went into the score’s assignment

How Are Risk Scores Calculated?

Risk scores are calculated by assigning a weighted score factor to each check that an automated underwriting tool performs. Those weights are based on things like the value of the data source and the importance to the user’s unique business risk policy. The score factors are then combined into a final number out of 100 and integrated into a wider risk scorecard that includes merchant details and information on any risk flags triggered.

Users can customize scoring by adjusting how specific items are weighted. For example, NMI ScanX allows users to adjust two types of weights:

- Scoring rule weights: How much each individual check contributes to the final risk score. For example, a specific database can be given extra weight if it has specific relevance for the user

- Page weights: How high-level groups of checks are weighted as a whole. For example, a user might want to boost the importance of a merchant’s combined credit checks or sanctions checks

Common Databases Used To Calculate Risk Scores

- GIACT (banking, identity and OFAC checks)

- TINCheck (business vitals, SSN and TIN verification)

- MATCH (terminated merchant checks)

- Experian Credit (credit reporting)

- TransUnion Credit (credit reporting)

- KYC SiteScan (KYB verification, webcrawl risk detection)

- LexisNexis (business and owner verification)

- Comply Advantage (AI-driven fraud and AML)

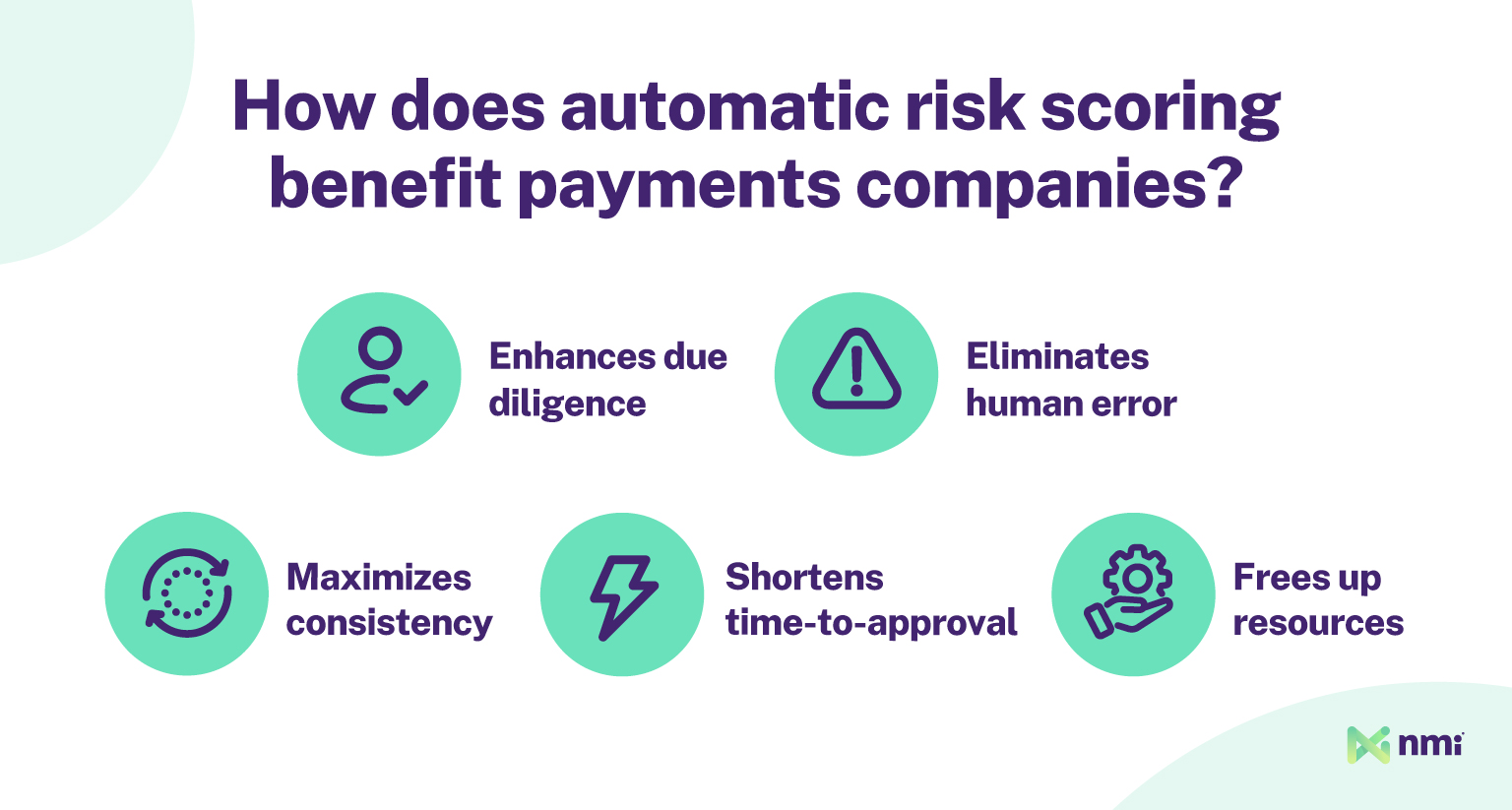

How Automatic Risk Scoring Benefits Payments Companies

Automatic underwriting tools and risk scoring benefit the due diligence process by augmenting human underwriters. The key benefits these systems offer include:

- Widening the underwriting net: Automated checks enable dozens of sources to be referenced in rapid succession, and risk scores make it possible to understand the results in seconds. That significantly expands the amount of due diligence an underwriting department can perform on each merchant, resulting in fewer risks slipping through the cracks

- Eliminating human error and maximizing consistency: The first big downfall of manual underwriting is consistency. Even at the best of times, checks regularly get missed, and results can be misinterpreted. Automated systems ensure every check is completed, and risk scores provide an objective metric that is applied consistently across every single merchant

- Shortening time-to-approval: The second major drawback of manual underwriting is speed. Thoroughly vetting a complex merchant application can take days or even weeks. Automated underwriting and risk scoring enable underwriters to run a complete set of checks, understand the results and make a decision in a matter of minutes

- Improving resource efficiency: Human underwriters are still the brain of the risk management process. Automated underwriting and risk scoring free underwriters from time-consuming, repetitive work on low-risk accounts. This allows them to spend more time analyzing and making tough decisions on more complex applications

Where Fast Approvals and Tight Risk Management Intersect

Automated risk scoring is one of the most effective tools available for speeding up underwriting and improving the consistency of results. However, fraud is evolving and skyrocketing at the same time that near-instant sign-up is becoming a critical competitive factor. As payments companies look to balance fast approvals and tight risk controls, reliable risk scoring will become even more important.

NMI offers two automated underwriting systems designed to help wholesale ISOs, PayFacs and other risk-handling payments companies find that balance.

ScanX is a fully automated underwriting system that offers over 100 checks against top underwriting sources. It offers high-customizability, automatic decision-making and reliable, accurate risk scoring.

MonitorX takes risk management beyond initial sign-up and maintains a constant watch over merchants. It regularly re-runs underwriting checks for the lifetime of the merchant’s processing and identifies any changes in behavior or information that might impact risk or pricing.

To find out more about how NMI’s automated underwriting suite can help you clamp down on risk while approving merchants more quickly, reach out to a member of our team today.