Your small merchants are facing uncertain times. Between inflation, tariffs, supply chain disruptions and labor shortages, it’s no surprise that the Small Business Optimism Index recently recorded one of its lowest readings in more than 50 years. On top of these pressures, many small merchants are also struggling to secure affordable capital — an issue that threatens their ability to weather these challenges and sustain long-term growth.

In difficult economic environments, small businesses often depend on loans and lines of credit to ensure they have enough working capital to pay suppliers, meet payroll and deal with emergencies. Unfortunately, a tough economy also means traditional lenders, like banks, are more risk-averse. That makes it more difficult for small businesses to access loans at the exact time they need them most.

The good news is that you can help them.

Embedded lending is an alternative way to give your merchants access to fast, easy and affordable loans directly inside your platform. Through a simple integration with a third-party lending partner, you can offer pre-approved loan options based on your merchants’ sales data, making capital available seamlessly.

So, let’s take a look at just how difficult access to capital has become for your small business customers, and how embedded lending solves the problem by giving them access to affordable capital when and where it’s needed, while also giving partners a simple way to earn additional, recurring revenue.

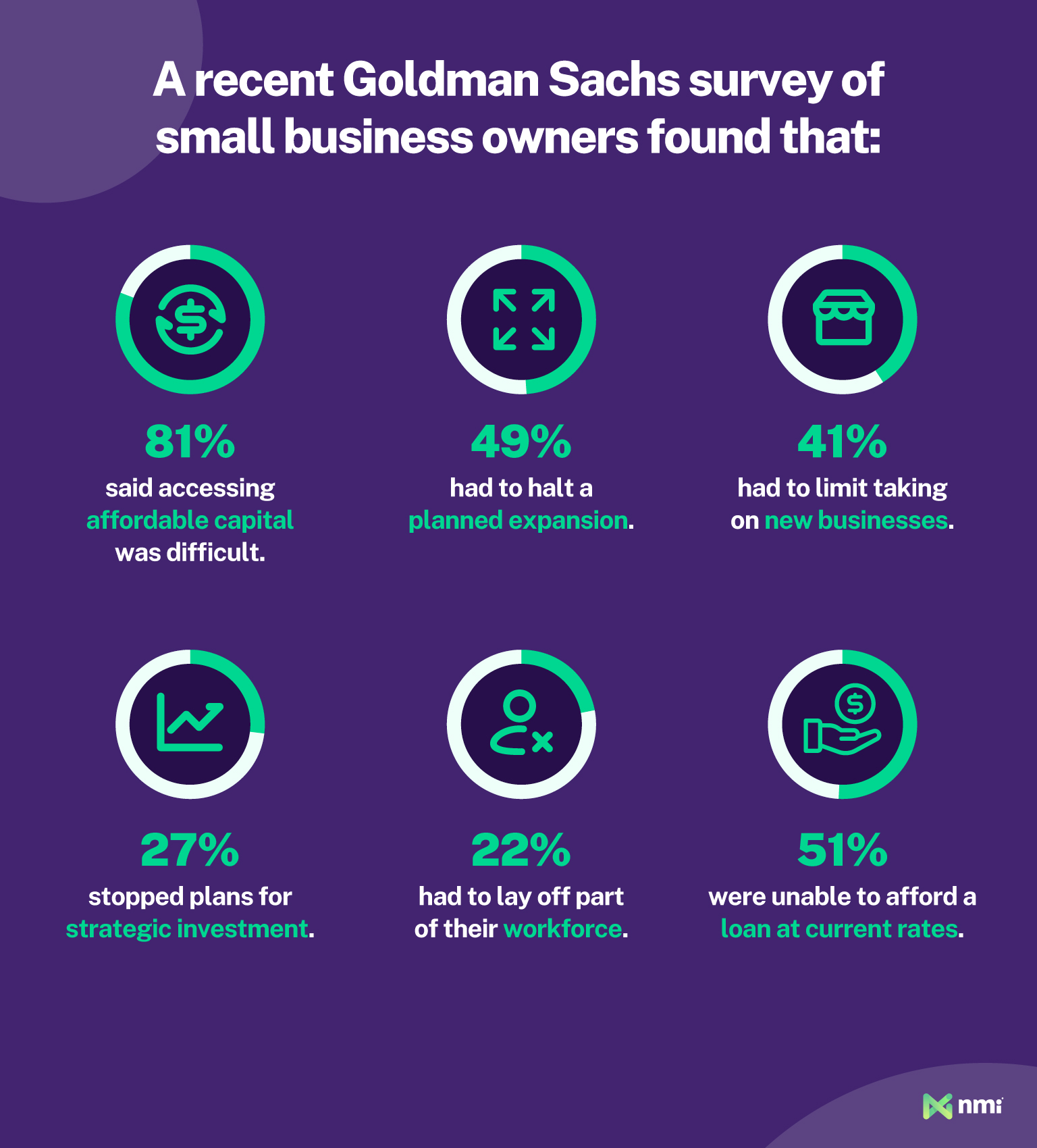

Accessing Capital Is a Major Challenge for Small Business Owners

Access to affordable capital is essential for small businesses, especially as the economic conditions tighten. But, far too many still struggle to secure the funding they need. In May 2025, Goldman Sachs surveyed small business owners who had applied for a business loan or line of credit in the previous year, and the results they found were alarming.

And relief is not on the way from traditional lenders. The Fed’s July 2025 Senior Loan Officer Opinion Survey found that banks are tightening requirements for small firms as their appetite for risk decreases. Loan sizes and maturities are shrinking, and covenants are becoming more restrictive, and these changes are hitting small businesses far harder than large or medium-sized firms. This signals a widening gap between the working capital small merchants need to navigate pressures like tariffs and inflation, and the willingness of financial institutions to provide it.

Embedded Lending: A New Way to Access Capital at the Point-of-Need

In many ways, the challenges small merchants face in today’s traditional lending environment stem from systems and processes that simply haven’t kept up with modern business needs. Embedded lending changes the dynamic because it takes advantage of two key strengths of modern fintech: direct platform integration and near-real-time data. Together, they enable three key advantages:

- The loan comes to the business owner — no need to search, apply elsewhere or navigate complex processes

- Qualification is based on recent, real performance data drawn directly from the platform, giving a far more accurate view of a merchant’s current financial health

- Performance-based assessment reduces traditional lending biases, helping level the playing field for small and underserved business owners

Embedded Lending Puts Pre-Approved Loans Just a Few Clicks Away

One of the most important advantages of embedded lending is the ability to deliver capital to the merchant right at the moment they need it. Instead of searching out a lender, filling out lengthy application forms and waiting days or weeks for a decision, a business owner can simply open the lending dashboard in their account and view any pre-approved loan offers already available to them. Accepting an offer typically takes a matter of minutes, and funds can be available in as little as a day.

The streamlined process embedded lending offers is especially important for small businesses because they often rely on loans for very different reasons than those of large corporations. For example, when an unexpected expense or emergency arises or a time-sensitive opportunity crops up, a small business can’t afford to spend days, or even weeks, going from bank to bank in search of a small loan. Embedded lending gives them fast, reliable access to the money they need to cover emergency expenses or take advantage of in-the-moment opportunities.

Embedded Lending Solves the “Black Box” Problem With Major Financial Institutions

The smaller a business is, the less likely it is to have extensive, up-to-date financial documentation available. That creates a “black box” situation, in which banks view small businesses as opaque and have a much harder time underwriting them than they do with larger applicants. This lack of visibility increases perceived risk, leading to higher interest rates, more stringent terms and a greater likelihood of being declined altogether.

In extreme cases, banks may struggle to verify even the simplest information. For example, research from PYMNTS found that almost 30% of microbusinesses have their loan applications declined because the bank can’t verify their basic data.

Embedded lending solves the black box problem by using real-time, in-platform sales data to make loan decisions. Small business owners don’t need to gather or submit detailed financial information because their loan offers are pre-approved based on their actual sales performance and ongoing revenue trends. This level of near-real-time visibility simply isn’t available to traditional lenders, and it gives embedded lending providers a significant advantage when it comes to underwriting and approving small and micro-sized businesses.

Embedded Lending Reduces Inherent Biases to Make Loans More Accessible to Minority Business Owners

Demographics can, unfortunately, play a big part in traditional business lending, and minority small business owners face even greater challenges than the broader small- and medium-sized business (SMB) community.

For instance, in 2024, research from Goldman Sachs found that 37% of Black-owned small businesses struggled to access capital. That’s 14% higher than non-Black owners. Black small business owners are also 9% more likely to worry about access to capital, 8% less likely to receive the requested funds, and 9% more likely to accept terms that they perceive as predatory.

Hispanic business owners face similar challenges, with research showing that 84% of Hispanic entrepreneurs are concerned about their ability to secure capital, underscoring how widespread and persistent these disparities are.

There are several reasons why minorities face a more difficult lending environment, including:

- Reduced access to local bank branches

- Fewer collateral options

- Stricter underwriting criteria

- Fewer banking relationships

- Misaligned incentives for financial institutions

By using sales data as the primary, or, in some cases, only determinant of loan eligibility, embedded lending helps break down many of these longstanding barriers. Embedded loan decisions don’t factor in an owner’s personal finances, age or socioeconomic status the way traditional lending often does. They also remove the need for in-person banking relationships or physical proximity to a branch. As a result, embedded lending helps level the playing field and makes capital more accessible for minority and underserved business owners.

What It All Means for Your Merchants

The unfortunate reality is that many of your small business customers are probably struggling to access the capital they need to grow and thrive — or even just stay afloat until economic conditions improve. Without access to that funding, day-to-day operations become harder, their long-term outlook is more uncertain and their revenue potential is significantly limited.

Embedded lending gives you a powerful way to support your small business customers by offering fast, easy access to affordable, pre-approved loans directly inside your platform. By making it simpler for your merchants to access the capital they need through small business loans, you unlock a true win-win situation in which their improved financial stability drives stronger performance, which in turn increases your residuals, adds a new passive revenue stream for your platform, deepens your value as a partner, and helps improve loyalty and reduce churn. NMI now offers frictionless embedded lending that can be integrated into your platform with the same speed and simplicity as all of our other products. To find out more about how embedded lending works, click here to read an in-depth article, or reach out to a member of our team to find out how easy it is to get started today.