Introduction: Why the Speed of Underwriting Now Defines the Merchant Experience

We all know instinctively that first impressions matter. In a self-serve world where small businesses sign up for payments without going through a traditional sales channel, your merchant onboarding process is often your first real touchpoint. How quickly and smoothly you get a merchant from signup to accepting payments sets the tone for everything that comes after.

So, what differentiates a great signup experience from a bad one? Today, it often comes down to your merchant underwriting workflow. Weeks-long underwriting was once the industry norm and every merchant knew to expect it. But that expectation has changed. Large platforms like Stripe and PayPal often allow merchants to start processing quickly while deeper checks continue in the background or after certain thresholds are met. For the merchant the experience feels almost instantaneous, even if underwriting is still happening behind the scenes.

That creates a challenge for providers that cannot afford to take the risk of delaying full underwriting. Merchants now expect fast onboarding, but providers still need strong risk controls. The good news is that speed is no longer exclusive to the biggest platforms. With modern underwriting tools, providers can perform real-time risk assessments on new merchants that are thorough, consistent and extremely fast. That means they can move quickly without cutting corners.

How Underwriting Automation Levels the Playing Field and Wins Better Merchants

Merchant expectations have changed. Speed and convenience are now competitive requirements. With faster underwriting and onboarding, you can compete with the biggest platforms while still offering the service quality, pricing and support that merchants value. Without that speed, underwriting becomes a source of delay between your merchants and their ultimate goal: selling. But underwriting faster means letting more risks slip through the cracks, right?

Underwriting has always been the biggest bottleneck in payments for one reason: humans are inherently bad at processing and analyzing large volumes of data at speed. Without risk management automation, underwriters had no choice but to manually verify dozens or even hundreds of data points for each application. That process is inefficient and inconsistent. The only way to improve accuracy and catch more risk was to slow down. But we don’t live in that world anymore.

Today, software is built for handling large volumes of data, especially as AI and automation become more advanced. Modern underwriting tools can run 100+ checks on every merchant, with no risk of fatigue or missed details. They can produce accurate, consistent risk assessments that don’t vary based on the underwriter, the day, or other factors that can affect manual decisions in tiny but impactful ways. And they can do it all in a matter of hours or even minutes instead of days or weeks, regardless of how much data needs to be reviewed or how complex the merchant’s risk profile may be.

This kind of data-driven underwriting and fully-automated risk scoring was once a major advantage that only the biggest platforms had access to – but not anymore. Now, it’s an equalizer that enables you to offer fast signup experiences while still outcompeting the big-name providers on things like service quality and pricing. And, as a result of the shift, a fast underwriting process, enabled by the right technology, is now actually a sign of better accuracy and consistency. So faster approvals no longer automatically mean higher risk. Often the exact opposite is true.

Automation Reduces Adverse Selection in Merchant Underwriting

Speed is not the only advantage of automated underwriting. It also helps providers attract better quality merchants.

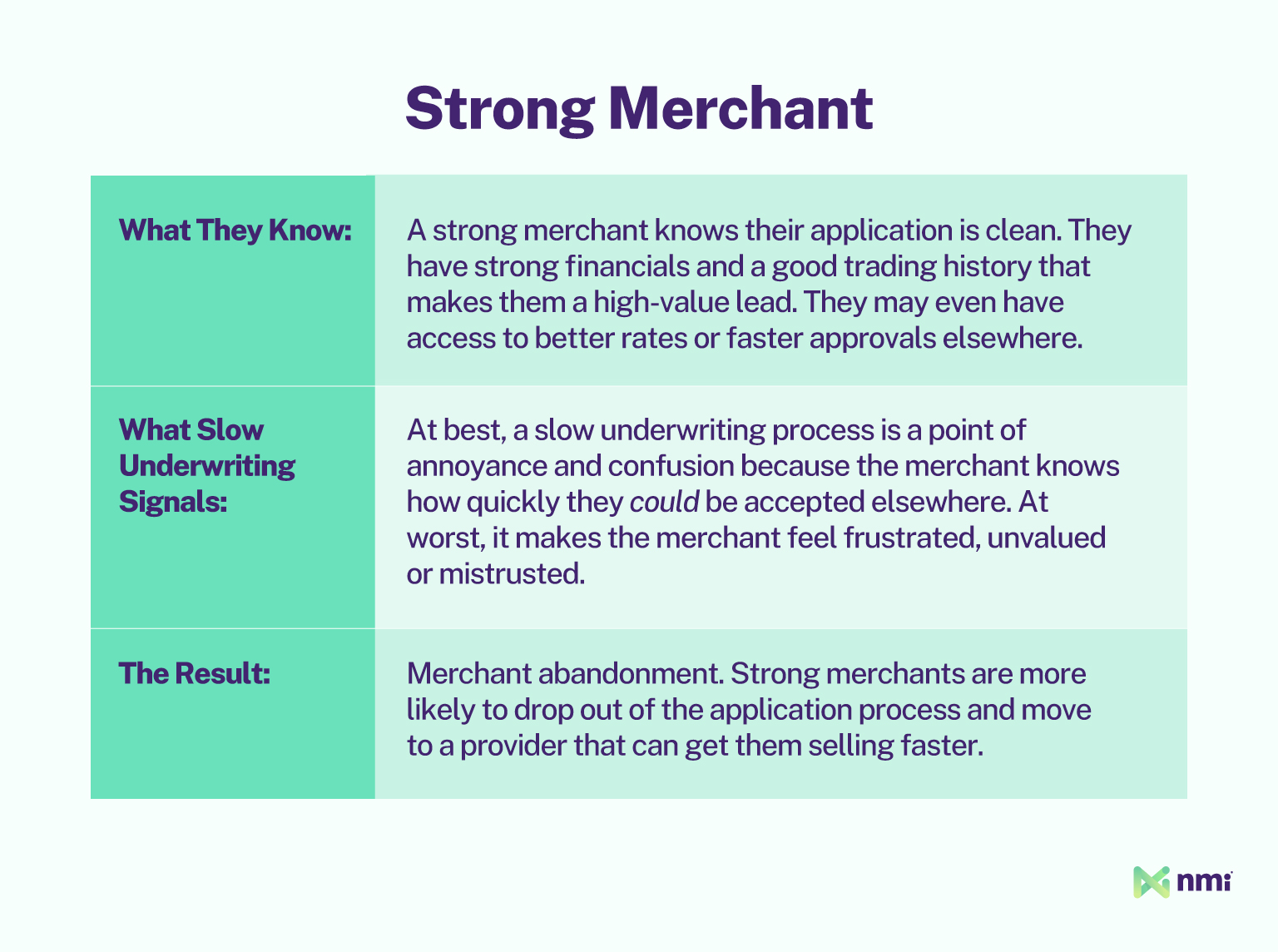

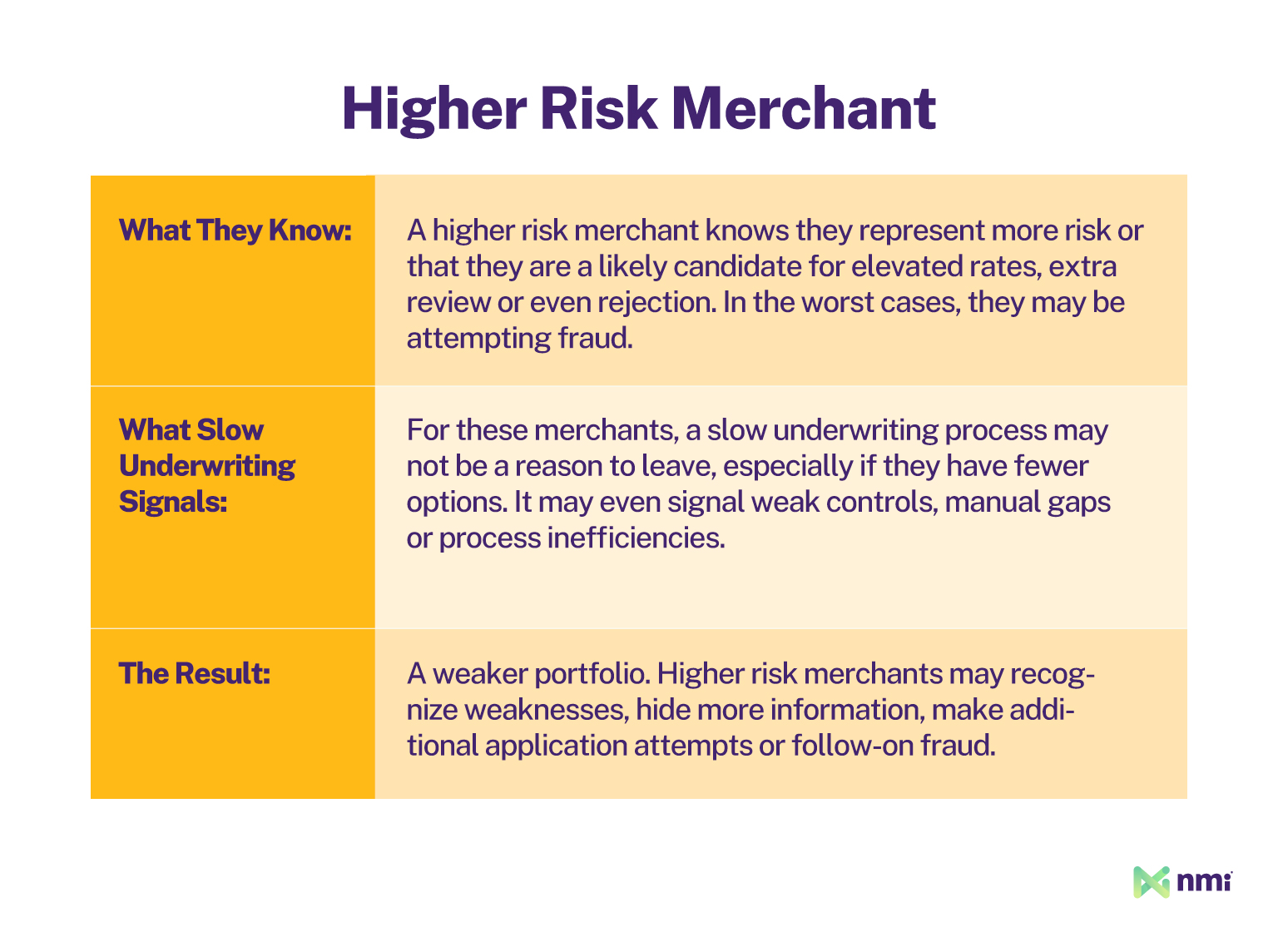

Adverse selection occurs when one party in a transaction knows more than the other and can use that information to its advantage. It’s a major issue in insurance, where applicants may hide pre-existing conditions that affect claims. It can affect payments underwriting too, for two main reasons:

- The riskiest merchants may hide details, misrepresent their business or disguise fraudulent intent

- The strongest merchants know they have options elsewhere

So, let’s think about what a slow, highly-manual underwriting process signals in each of these cases.

Slow underwriting can drive away the merchants you most want to win and leave you with more of the risk you are trying to avoid. Over time that can damage your portfolio quality and increase exposure to fraud, chargebacks and losses.

By automating your underwriting, you can significantly reduce that risk. Speed keeps the best merchants from jumping ship midway through an application, while fast and consistent identification of yellow and red flags helps show higher-risk applicants that weak or incomplete applications will be caught quickly..

Open Banking is Driving a New Era of Even Faster Underwriting

Automated checks and risk assessments already accelerate underwriting. But now, open banking integrations are pushing speed even further by making account and identity verification faster and more reliable.

Open banking allows the underwriting system to pull critical account data directly from the merchant’s bank via a secure, read-only API connection. It’s completely optional, but merchants that choose to authorize it can speed up their onboarding in a number of ways, including:

Reduced signup friction: Open banking gives underwriters a direct connection to trusted financial data, which completely eliminates the need for the merchant to upload large numbers of financial statements. That speeds up signup and helps create a great first impression.

Faster identity and bank account verification: Because the data comes directly from the bank, account ownership and history can be verified quickly. That reduces downstream checks, cuts manual document review and reduces the potential for fraud significantly.

Access to real-time financial data: direct access to current bank records enables fast, accurate revenue validation and better visibility into everything from cash flow to daily balances and other important financial signals. That supports faster approvals and more accurate pricing.

Together these benefits enable faster, higher-quality underwriting and a better merchant experience. Open Banking can also provide an additional trust signal.. A merchant that agrees to share verified bank data is far less likely to be hiding fraudulent intentions, while merchants that decline may require further review depending on the wider risk profile

Setting a New Standard for Underwriting in 2026 and Beyond

Fast underwriting is no longer just about operational efficiency. It is now part of how providers compete, manage risk and build healthier merchant portfolios.

Human underwriters will always be a critical part of assessing complex risk, but the era of manual-first underwriting is over. To compete with the biggest platforms and attract the best merchants, providers need underwriting that is fast, automated and consistent. The question is how to move faster without sacrificing quality; the answer is NMI ScanX.

ScanX is an advanced automated underwriting system that reduces both risk and time-to-processing. It can reduce underwriting time from days or weeks to hours or even minutes, while supporting thorough due diligence through:

- Customizable rules-based scoring

- Identity and watchlist verification through TINCheck

- Automated KYC and AML through KYCSiteScan

- Open banking integration for API-driven data collection and verification

- Accurate, consistent, automatic or human-in-the-loop decisioning

- Automatic in-depth decision report generation

- Frictionless integration with NMI Merchant Central payments CRM

To find out more about how ScanX can boost your underwriting speed and help you win better merchants, reach out to a member of our team or download our white paper, Why Automated Merchant Onboarding and Underwriting is Table Stakes.